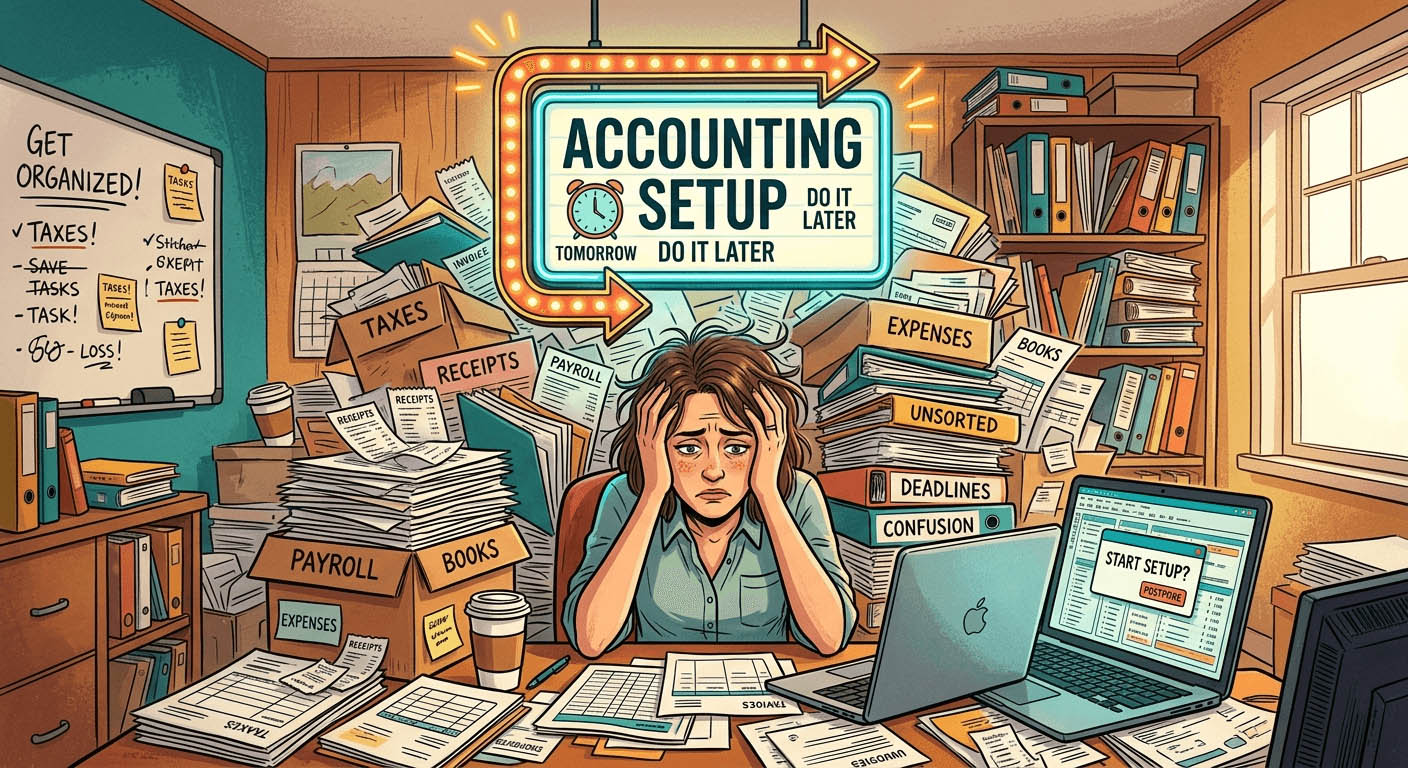

Tax season arrives and suddenly the receipts come out. The folders get opened. The spreadsheets get dusted off. For millions of small business owners across American cities, this is the moment bookkeeping becomes real. Not in January. Not in July. In April, when the deadline is breathing down their necks. If that sounds familiar, you are not alone, but you are costing yourself more than you realize.

The Bottom Line Before You Read On

Delaying your accounting setup does not save time. It costs time, money, and mental energy every single year. Owners who get their books in order early spend less at tax time, catch profit leaks faster, and make better decisions with real numbers. The setup itself is not complicated. The avoidance is the problem.

Why Bookkeeping Always Ends Up at the Bottom of the List

Small business owners are busy people. There are customers to serve, products to move, and staff to manage. Bookkeeping does not feel urgent until it suddenly is. This is the classic tension between what is important and what is pressing.

Running a shop in Chicago or a service business in Austin means your days are full of visible, tangible work. Logging expenses and reconciling accounts feels abstract by comparison. The numbers do not change the moment you record them, so it is easy to assume recording them can wait.

But here is what happens when it waits. Receipts pile up. Categories blur. You forget what that $340 charge was in August. By the time your accountant asks, you are guessing. And guessing costs money, either through missed deductions or inflated taxable income.

The solution is not willpower. It is structure. Building the right accounting setup early in the year, or even right now, is the single highest-leverage thing most small business owners can do for their financial health.

Core Accounting Is the Foundation, Not an Optional Add-On

Most owners think of accounting as reporting, something that produces documents at the end of a period. In reality, core accounting is the live operational layer underneath your business. It tracks what comes in, what goes out, what you owe, and what you are owed, in real time.

When that layer is working properly, your business produces accurate numbers automatically. You are not scrambling to reconstruct transactions. You are reading a clear picture of where you stand.

For a small business owner in any American city, that picture matters more than most people admit. It is how you know whether you can afford to hire a part-time assistant. It is how you spot a client who is consistently late on payments. It is how you see that your material costs crept up by 12% over six months while your prices stayed flat.

Without a functioning accounting setup, all of that is invisible. You are running your business on instinct, which works until it does not.

Setting Up Your Books Before Things Get Messy

The best time to set up proper accounting is before you need it. The second best time is now. Here is a numbered approach that helps owners start from a stable base rather than digging out from chaos:

- Open a dedicated business bank account if you have not already. Mixing personal and business finances is one of the most common and costly mistakes small owners make.

- Choose an accounting method. Cash-basis is simpler and works for most small operations. Accrual gives a more accurate picture of profitability over time. Know which one you are using.

- Set up a chart of accounts. This is simply a list of categories: income, cost of goods sold, operating expenses, and so on. It does not need to be complicated, just consistent.

- Connect your bank and card accounts to your accounting software so transactions import automatically. Manual entry is where things fall apart.

- Schedule a weekly 20-minute bookkeeping block. Categorize imports, flag anything unusual, and check your balances. Twenty minutes weekly beats eight hours in April.

- Reconcile monthly. Match your software records against your actual bank statements every month. This catches errors, duplicates, and fraud early.

How Messy Receipts Inflate Your Costs and Distort Your Profits

Here is a scenario that plays out in small businesses every single year. An owner pulls together their annual numbers and is shocked to find expenses far higher than expected. The culprit is usually not one big cost. It is dozens of small, uncategorized, undocumented transactions that got lumped into a vague bucket.

When receipts are disorganized, two things happen. First, deductible expenses go unclaimed because they cannot be matched to a category. Second, personal purchases occasionally slip into business totals, inflating your cost of operations and making profit look lower than it actually is.

Consistent expense tracking fixes this. Not by adding bureaucracy, but by creating a record of what actually happened. When every transaction has a home, your numbers stop being estimates and start being facts.

For a business owner in, say, Denver or Nashville, the tax implications alone can be significant. Missed deductions mean higher taxable income. Higher taxable income means a bigger bill. The tracking habit pays for itself.

The Expenses That Most Owners Miss

Some costs are obvious: rent, payroll, inventory. Others slip through. Here are the categories small business owners most commonly under-document:

- Mileage and vehicle use for business travel

- Home office expenses if you work from home part of the time

- Software subscriptions billed annually and then forgotten

- Professional development, courses, and books

- Bank fees and merchant processing charges

- Meals with clients or business partners

- Equipment purchases that qualify for depreciation

- Professional services like legal, design, or consulting

None of these are exotic. They are ordinary costs that reduce taxable income. But only when they are recorded.

What Good Books Actually Tell You Day-to-Day

Clean, current books are not just a tax tool. They are a management tool. Here is what owners with well-maintained books can answer at any point during the year without calling their accountant:

- Am I profitable this month, and how does that compare to last month?

- Which product line or service is actually making money?

- Are my operating costs increasing as a percentage of revenue?

- Do I have enough cash to cover next month’s obligations?

- Is a specific client costing me more to serve than I earn from them?

Answering these questions with confidence changes how you run your business. It shifts you from reactive to proactive. You are not waiting for a crisis to look at your numbers. You are using your numbers to prevent the crisis.

Using Calculators to Sanity-Check Your Margins Without an Accountant

Not every financial question requires a professional. Many of the most useful calculations are straightforward, and you can run them yourself in minutes. Financial calculators give owners a fast way to check their break-even point, test pricing scenarios, or project cash flow without opening a spreadsheet from scratch.

Break-even analysis, for example, tells you exactly how much revenue you need to cover your fixed costs before you start making a profit. Knowing this number changes how you price, how you plan your sales targets, and whether a slow month is a real problem or just normal variation.

Margin calculators help you see whether a price increase actually improves profit or just inflates revenue while costs eat the difference. Owners who run these checks regularly tend to make better pricing decisions than those who guess based on gut feel.

These tools are not a replacement for professional advice on complex matters. But they are a way to stay informed and engaged with your numbers between accounting reviews. For owners in competitive markets, across cities like Atlanta, Phoenix, or Seattle, that kind of real-time awareness is a genuine advantage.

A Simple Framework for Using Calculators Effectively

You do not need to run every calculation every week. A useful rhythm looks like this:

- Monthly: Check your gross margin. Is it holding steady or sliding?

- Quarterly: Re-run your break-even analysis with current cost figures.

- Before any big decision: Model the financial impact before you commit. New hire, new product, new pricing structure. Run the numbers first.

The Year-Round Habit That Changes Everything

The owners who feel least stressed at tax time are not necessarily the most organized people in the world. They are simply the ones who made accounting a weekly habit rather than an annual event.

Twenty minutes a week. Monthly reconciliation. Consistent expense categories. A reliable way to check your margins when you need to. That is the entire setup. It is not complicated. It is just consistent.

If you have been running your business on instinct and hoping the numbers work out, this is the moment to change that. Not because tax season is coming. Because you deserve to know how your business is actually doing, right now, with real numbers you can act on.

The fire drill is optional. The numbers are always there. The only question is whether you are looking at them.